However, much progress has been made in more transparent explanations of the operation of financial products.

Due to the fact that, in the past few years, the customer database within the financial institutions has clearly been segmented, a greater trend has come about for more relationship banking. Financial advisors have been able to specialise in a specific customer profile. That must enable them to explain the products and services they propose in a clear and understandable manner adapted to the customer.

Saving products

On 13 July 2012 an agreement in principle was concluded between Johan Vande Lanotte, Deputy Prime Minister and Minister for the Economy, Consumers and the North Sea, Steven Vanackere, Deputy Prime Minister and Minister for of Finance, the FSMA supervising body and Febelfin. One of the things the agreement provides for is that for each regulated savings account a standardised information sheet must be drawn up on which all essential information appears. That way the consumer will be able to compare the saving products of the various financial institutions easily.

Investment products

An information sheet must be provided not only for the savings account but also for investment products , which may only supplied with such a sheet, the KIID (key investor information document). This sheet provides information on the key aspects of the investment product as well as the risks and costs associated with the product. Each KIID is subject to the same standard in terms of the structure, content and presentation. This will allow consumers to compare various investment products and ultimately choose the product that best meets their needs.

The MiFID directive also aims for better protection of the investor. MiFID provides that a financial advisor cannot sell investment products to a customer if they do not match the customer’s investor profile. Each year a test must be done to see if a customer’s investment products match his profile.

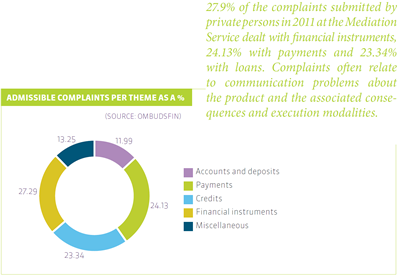

In the framework of the simplification of products, great progress was made via the moratorium on the commercialisation of especially complicated financial products. The financial sector has voluntarily endorsed the moratorium, which obliges it not to commercialise any structured products that are defined as especially complicated by the Financial Services and Markets Authority (FSMA).

Loan products

The Consumer Credit Protection Act imposes the use of the “JKP” (jaarlijks kostenpercentage or annual percentage rate of charge, which denotes how much a loan costs on an annual basis). This provides the consumer with the possibility to compare various offers easily and prevents him from being confronted with “unclear calculation keys”.

The legislation also provides that advertisements about loans (in which an interest rate is not mentioned) must be accompanied with the message “Pay attention: borrowing money also costs money”.

Both for corporate loans and for private loans, a code of conduct exists in which transparency is stated as one of the values.

The 2004 the Code of conduct for lending was signed between banks and businesses[1]. Improvement of transparency is one of the most important assignments of the Business Financing dialogue platform, which was established to re-establish confidence in the sector. The Platform does this for instance via the Business Financing website.

On this site, entrepreneurs can find information and tips to give their loan application the best possible chance. On the site they can also find information about governmental initiatives in respect of funding, information about ratings, etc.

When a loan request is rejected, the banks, in accordance with the Code of Conduct, must explain the main factors that affected their loan decision. Giving a second chance is a crucial point for attention: when a loan is not granted but the proposed project is viable, the banks will consider on their own initiative how the proposal may be adjusted.

Since the beginning of 2000 the Consumer Loan Guide, the corresponding budget table and the brochure about home loans have been available[2].On the site of the Professional Association of Credit Providers (Beroepsvereniging van het Krediet –BVK/Union Professionnelle du Crédit - UPC), a sub-association of Febelfin. These instruments offer private individuals a complete overview of loans and help them to make a proper assessment of their payment capacity.

[1] The Code of Conduct can be viewed on www.financieringvanondernemingen.be.

[2] For the guides and brochures see www.upc-bvk.be.